The Property Insurance Market in 2026: Turning Renewals Into a Data-Driven Conversation

Insured AI Team

Most multifamily owners already have the data they need to win a better insurance renewal. They just can't act on it.

Walk into any mid-sized owner-operator and you'll find years of policies, loss runs, inspection reports, vendor certificates, rent rolls, and claim files.The information exists, but it's scattered across emails, drives, and shared folders, in formats no one has time to reconcile. What's missing is the analytics layer that turns it into internal benchmarks and actionable trends - the story underwriters and lenders actually price against.

In the 2026 softening property market, that gap is what separates owners who use the cycle to reset their programs from those who watch the window close at the next renewal.

The data is in the building. The analytics aren't.

A typical 40-property multifamily portfolio generates hundreds of insurance-relevant documents every year. Policies across four or five lines. Loss runs from multiple carriers. Inspection reports, capital expenditure logs, certificates of insurance, crime-score updates, and rent rolls that quietly change insured values on every asset.

But no holistic view. Brokers see one renewal at a time. Asset managers see financial performance but not loss frequency. Property managers see incidents but not portfolio-wide patterns. The owner ends up with a stack of PDFs and a quote they can't meaningfully challenge.

That isn't a documentation problem. It's an analytics problem.

Internal benchmarking is the leverage most owners never use

External market benchmarks - what similar portfolios pay, what the industry average looks like - are table stakes. Every broker brings them. They rarely move a renewal, because the underwriter has already run the same comps.

Internal benchmarking changes the conversation. When an owner can show that water-damage frequency dropped 41% across garden-style assets after a valve replacement program, or that slip-and-fall claims clustered around two vendors since replaced, the discussion stops being about rate. It starts being about a different risk than the underwriter originally modeled.

That shift only happens when a portfolio's own data is normalized, comparable, and trended over time - across properties, across years, across carriers.

Three trends hiding in every portfolio

Three patterns show up in almost every multifamily book, and almost nobody pulls them out:

- Exclusion creep. Assault & battery sublimits that were $5M two renewals ago are often $2M today, sometimes $1M - and the change gets buried in binder language rather than the declarations page. Owners rarely see it until a claim hits the sublimit.

- Replacement-cost drift. Renovations push insured values up, but valuation refreshes lag. On wood-frame assets, many portfolios are insured 15–25% below current rebuild cost without realizing it.

- Retention curves out of alignment with frequency. A property retaining the first $100,000 per claim while averaging four mid-sized losses a year is self-insuring at a worse effective rate than the open market would charge.

Each of these patterns is visible in data owners already have. None of them are visible in the way that data is currently organized.

What the 2026 market actually rewards

The 2026 cycle is unusual: property rates are softening while liability is tightening, and surplus markets are absorbing most of the multifamily risk that mainstream carriers used to write (per Marsh McLennan's 2026 real estate risk report). Nonrenewal risk on aging or higher-crime assets is climbing, and exclusions around A&B, habitability, and punitive damages are showing up more often in standard forms.

The practical effect: the gap between a well-prepared renewal and a poorly-prepared one is widening fast. A portfolio walking in with normalized loss history, current valuations, documented remediation, and a clear exclusion inventory is pricing against a different curve than one walking in with binders and a broker deck.

Rate shopping cannot close that gap. Analytics can.

What a comprehensive analytics layer actually does

An analytics layer built on top of a multifamily insurance portfolio does four things that a broker relationship alone can't:

- Centralizes and structures every insurance-relevant document, so policy terms, loss data, valuations, and operational records are queryable in one place.

- Detects exclusions and gaps - the shrinking A&B sublimit, the new habitability exclusion, the LIHTC endorsement that never got added - before they become compliance or claims problems.

- Benchmarks internally across properties, years, and carriers, so operational changes are measurable as risk changes, not just capex line items.

- Surfaces trends early - frequency clustering, vendor-driven claim concentrations, retention mismatches, valuation drift - while there's still time to act before renewal.

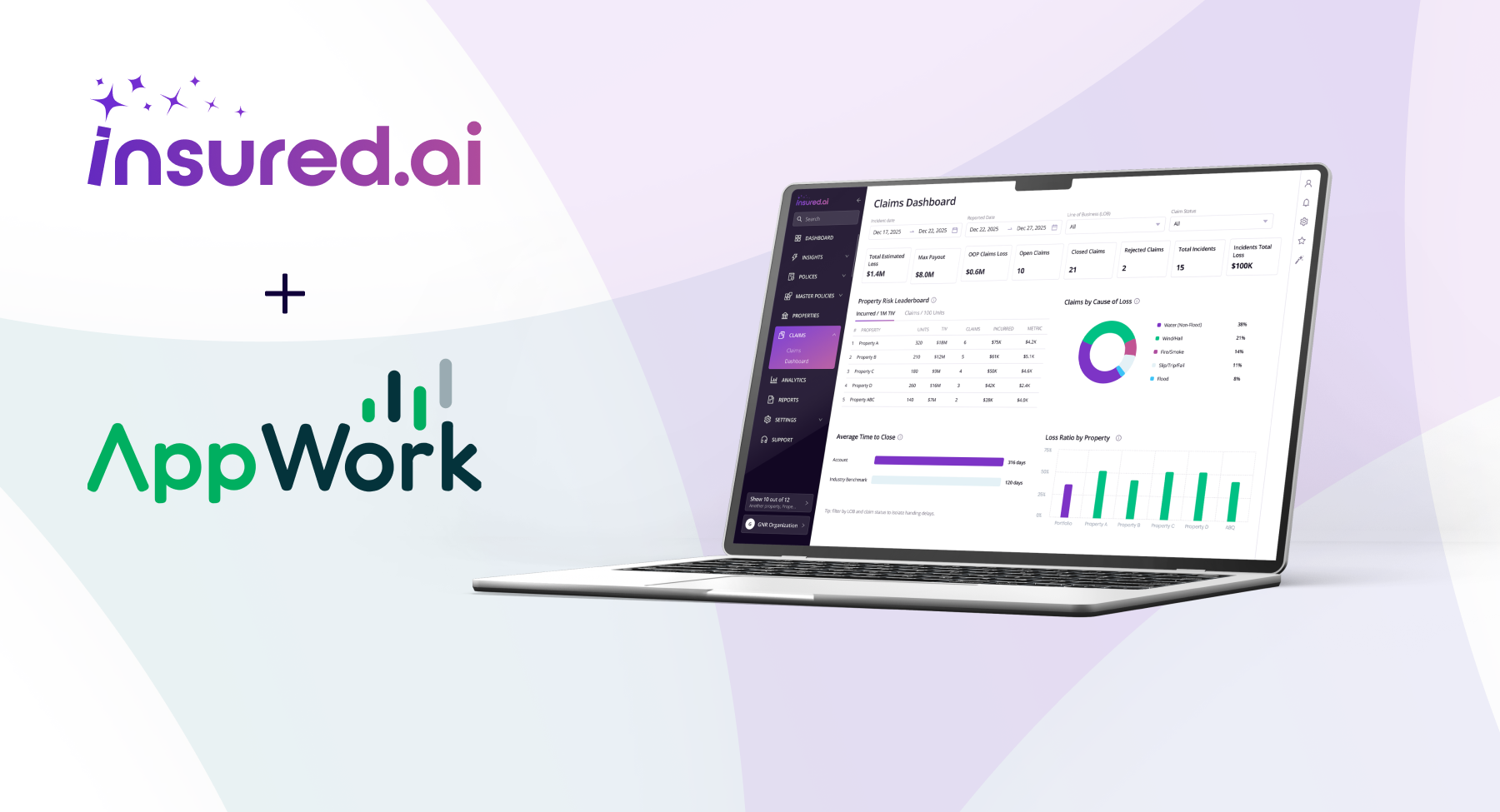

This is what Insured AI was built to do: turn fragmented insurance documentation into a continuous, analytical view of risk that owners, asset managers, and brokers all work from.

The renewal changes when the data does

The multifamily owners who will navigate 2026 best aren't the ones with the sharpest brokers. They're the ones who walk into every conversation - with carriers, lenders, and brokers - already knowing what their own portfolio says.

That is what comprehensive analytics actually delivers: internal benchmarks that can't be argued with, actionable trends that convert into better terms, and a renewal story that doesn't depend on anyone else's framing.

.png)