Multifamily Insurance Compliance: What Property Owners, Managers, and Lenders Need to Know

Insured AI Team

Insurance compliance in multifamily is one of those areas that feels manageable - until it isn't. A missed certificate, a lender requirement buried in a loan agreement, or a coverage gap discovered during an acquisition can trigger forced-placed insurance, loan default notices, or worse, an uninsured loss.

This guide covers the five compliance areas that consistently catch multifamily operators off guard - and what to do about each one.

Forced-Placed Insurance: What Triggers It and How to Avoid It

Forced-placed insurance - also called lender-placed insurance - occurs when a lender determines that a borrower's property insurance has lapsed, fallen below required coverage levels, or failed to name the lender as an additional insured. The lender then purchases a policy on the borrower's behalf and charges the cost back to them.

The result is almost always unfavorable. Forced-placed policies are significantly more expensive than market-rate coverage, often provide less protection, and exist solely to protect the lender's collateral interest - not the owner's.

Common triggers

- Policy expiration without timely renewal evidence

- Coverage limits that fall below the loan agreement threshold

- Failure to list the lender or servicer as an additional insured or loss payee

- Policy cancellation due to non-payment or underwriting issues

How to avoid it: The single most effective prevention is proactive certificate management - ensuring that updated COIs are delivered to lenders before expiration, not after. Tracking renewal dates, lender notification requirements, and coverage minimums across a portfolio is where most operators fall short.

Certificate of Insurance (COI) Management Across a Growing Portfolio

A certificate of insurance is a snapshot of your coverage at a point in time. The problem is that lenders, property managers, investors, and tenants all require them - and they expire. Across a growing portfolio, COI management quickly becomes one of the most administratively demanding compliance functions in the business.

The operational risks are real. An expired COI submitted to a lender can trigger a forced-placement event. A COI that doesn't reflect current coverage terms can create a compliance gap that only surfaces during a claim or audit.

What good COI management looks like:

- A centralized tracker for every certificate issued, to whom, and when it expires

- Automated renewal reminders tied to policy expiration dates

- Version control - ensuring that the COI on file with each party reflects the current policy, not last year's

- A clear process for updating certificates when coverage changes mid-term

For operators managing five or more properties, manual COI tracking in spreadsheets is a liability. The volume of certificates, parties, and expiration dates creates too many failure points.

Lender Insurance Requirements vs. What You Actually Carry - Spotting the Gaps Before They Spot You

Every loan agreement contains insurance requirements. Most borrowers review them at closing and never look again. The problem is that coverage needs to evolve - construction costs rise, liability exposure shifts, and lender requirements change at refinance - while policies often don't keep pace.

The most common mismatches:

- Replacement cost coverage that has not been updated since origination, now below lender minimums

- Liability limits that met requirements at closing but fall short of current loan terms

- Missing endorsements - flood, ordinance and law, or loss of rents - that the loan agreement requires but the policy doesn't include

- Lender not listed correctly as additional insured or loss payee on the current policy

The fix: Pull your loan agreements and compare the insurance requirements line by line against your current policy declarations and endorsements - not your memory of what you bought three years ago. Do this at every renewal and at every refinance. Gaps found proactively cost nothing. Gaps found by your lender or after a claim can be material.

Common Compliance Pitfalls When Acquiring a New Multifamily Property

Acquisitions introduce a compressed window where compliance risk is highest. Insurance requirements must be met at closing, existing policies must be reviewed and often replaced, and new lender requirements come into effect immediately.

Where acquisitions go wrong:

- Binding coverage based on seller-provided data that turns out to be inaccurate - wrong square footage, undisclosed loss history, or misrepresented construction type

- Assuming the existing policy transfers cleanly when it doesn't

- Missing the lender's required endorsements because they weren't flagged during due diligence

- Failing to update the named insured, additional insured, and loss payee designations before closing

Best practice: Treat insurance compliance as part of your due diligence checklist, not a closing-day task. Review the existing policy, request five years of loss runs, confirm lender requirements early, and build in enough time to bind proper coverage before the transaction closes.

The Most Common Compliance Gaps in Multifamily Portfolios

Across multifamily portfolios of all sizes, the same compliance gaps surface repeatedly:

Outdated replacement cost valuations - Replacement costs that haven't been updated in two or more years are frequently below both lender minimums and actual rebuild exposure, creating simultaneous compliance and coverage risk.

Missing or incorrect additional insured designations - Lenders, property managers, and investors often need to be listed specifically. A policy that names the wrong entity or uses an outdated legal name can void a lender's protection and trigger a compliance event.

Lapsed or untracked umbrella policies - When an umbrella policy lapses or isn't renewed on the same schedule as the underlying policy, it can create a gap that neither the insured nor the lender catches until it's too late.

No documented compliance process - The most pervasive gap isn't a specific coverage issue - it's the absence of a system. Operators who manage compliance reactively, responding to lender requests rather than getting ahead of them, consistently find themselves in situations that could have been avoided.

Compliance Is a System, Not a Checklist

Insurance compliance across a multifamily portfolio isn't something you solve once. It requires ongoing visibility into policy status, certificate currency, lender requirements, and coverage adequacy - across every asset, every lender, and every renewal cycle.

Operators who treat it as a system - with centralized data, proactive tracking, and regular gap analysis - avoid the costly surprises. Those who don't tend to discover their gaps at the worst possible moment.

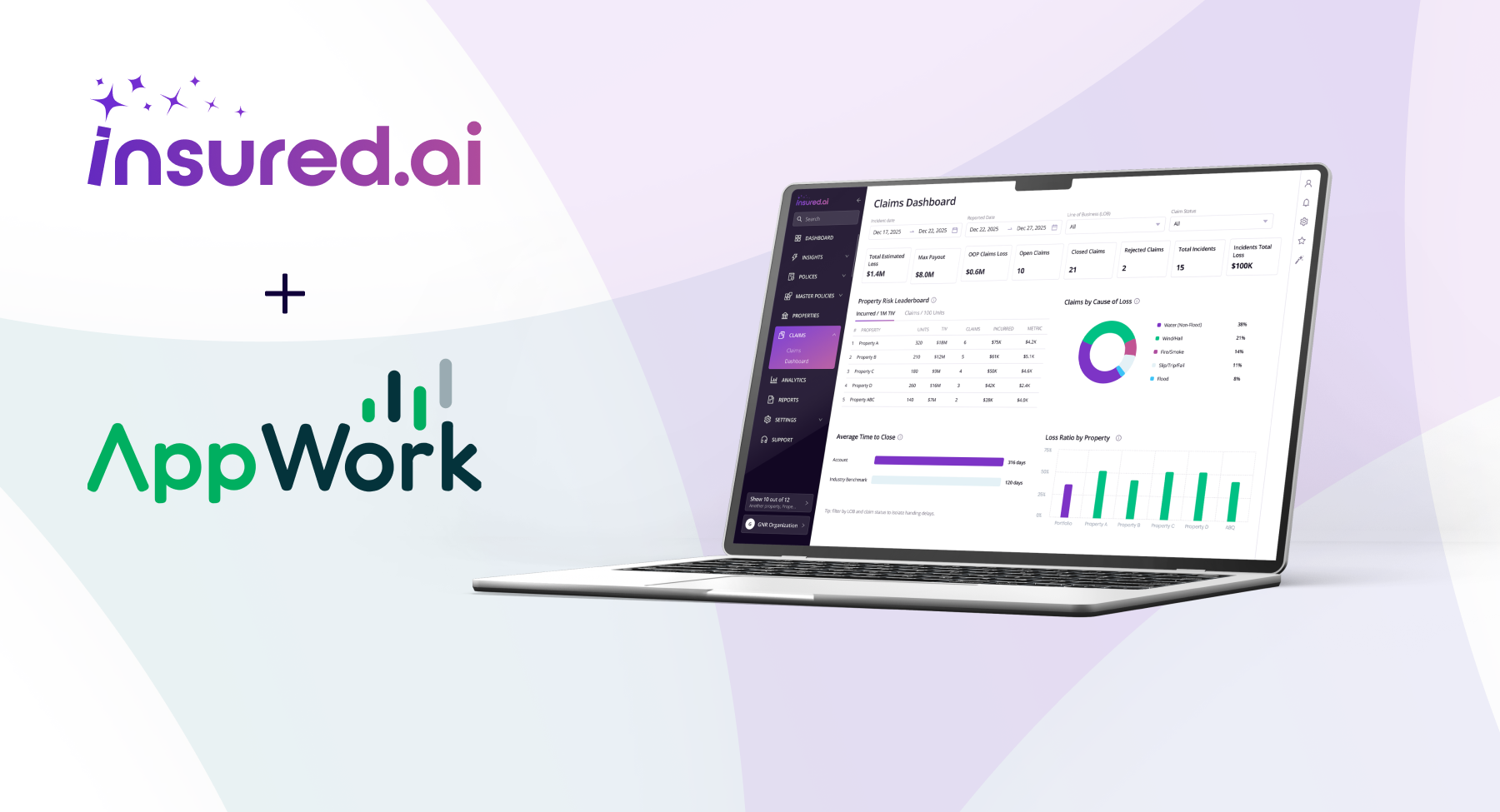

Insured AI gives multifamily owners, managers, developers, and lenders a single platform to track coverage compliance across every property - surfacing gaps, flagging upcoming renewals, and ensuring that what's on file with your lenders actually matches what you carry.

.png)